Unveiling Ebix's 10x Upside Through Bankruptcy

Ebix Equity is a Mispriced Option, Accounting Gimmicks and Bankruptcy Dynamics Obscure Fundamental Value and Free Cash Flow Generation

Ebix Inc (EBIXQ)

May 6, 2024

Ebix is a small conglomerate with insurance-related businesses in the US and a foreign exchange business in India

Ebix filed for bankruptcy on December 18th in the Northern District of Texas; it is expected to emerge in September

Deceptive accounting hides a solid business

After selling its main business in a post-petition sale, Ebix is trading at 4x EV/EBITDA

Multiple paths to exit bankruptcy leave a decent chance of retaining equity value

Background Overview

Ebix is a small conglomerate that looked like a high-quality compounder for most of the last 20 years. This changed after it took out too much debt to pursue an Indian rollup. Short sellers highlighted its deceptive accounting and lobbied Indian regulators to filibuster the proposed spinoff of its Indian business. The company tried to play hardball with creditors. However, after 15 amendments to its credit agreement, the creditors lost patience and forced it into bankruptcy.

Since filing in December, Ebix has announced the sale of its core US business and now carries ~3x Net Debt/EBITDA. To invest in Ebix, you must believe 1) that its remaining segments are real cash-flowing businesses (not total frauds) and 2) that they are worth more than 4x EBITDA. If both those things are true, there is a high likelihood of full equity value retention.

Why does this opportunity exist?

Forced selling from all ETFs post-bankruptcy and delisting

No natural buyers

Distressed funds are not looking at this situation because the debt is closely held by the banks

Microcap equity investors generally do not have distressed experience

Protections to prevent a change in control wiping out the NOLs mean new shareholders must declare their intent to buy more than 4.5% of a company and wait 20 days, limiting position size to ~$1M

Accounting irregularities and businesses in niche overseas industries add to the complexity

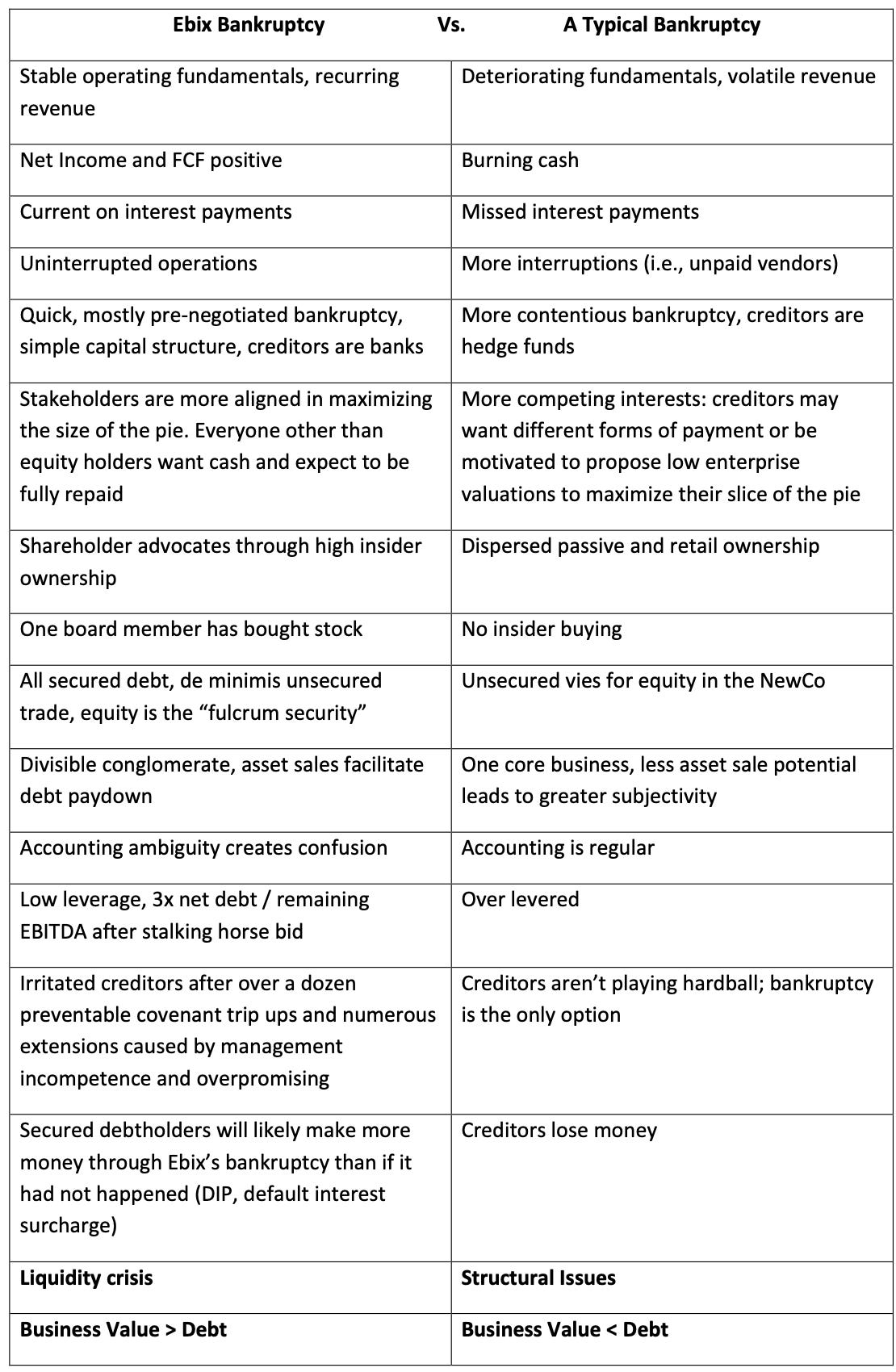

How is this bankruptcy different from most bankruptcies?

Ebix’s main business segments are:

Life and Annuity Insurance Exchanges (NA L&A): Ebix owns insurance exchanges that facilitate interaction between carriers and brokers, mainly in the life and annuity verticals. This business was sold to Zinnia in a $386.5M Stalking Horse Sale.

International Insurance Exchanges: Ebix has an 80% market share in its Brazilian and Australian P&C exchanges. These are very steady, high-margin businesses, albeit low-growth ones.

EbixRCS Risk Compliance Solutions: EbixRCS furnishes insurance certificate tracking and compliance software for clients to manage vendor documentation. It also has a small P&C solutions segment.

EbixCash: EbixCash is the retail agent (like being a master franchisor) covering 60% of Western Union’s Indian remittance business. It handles an even more significant proportion of MoneyGram and Ria’s networks. It has spent a decade and $700M to build this irreplicable distribution network with tens of thousands of distribution outlets (mainly mom-and-pop shops) in every rural town and major city in India. A strategic acquirer may find vale in cross-selling other financial products through this distribution network.

EbixCash also owns the largest airport foreign-exchange kiosk operator in India and participates in other payment verticals like overseas university tuition payment, bus ticket processing, and utility payment processing.

Finally, EbixCash’s best business is its travel business. It has a B2B travel and Meetings, Incentives, Conferences, and Exhibitions (MICE) segment as well as a consumer facing online/offline travel agency. Though this segment is intertwined with the forex business (they cross-sell ), the most recent periodic report indicates that it has grown from 33% YoY to ~$40M in LTM revenue.

Other NA Assets: Ebix spent $100M acquiring Oakstone and A.D.A.M., a medical publishing and continuing medical education business. It also has a consulting division, a third-party administrator (TPA), an employee benefits enrollment and administration software business. These businesses are small, mismanaged and deteriorating. They will sell but not for much.

While Ebix's revenue in its remaining NA businesses is declining, growth in India serves as a counterbalance. The growth in India becomes even more significant when considering forex headwinds and business mix improvements, characterized by fast growth in its high-margin travel business and a withdrawal in its low-margin pre-paid card business.

Collectively, Ebix’s businesses earn very good returns on capital. Before the NA L&A sale, Ebix historically made ~$100M in UFCF off ~$250M of tangible assets.

Accounting Reconciliation

The most important thing to note in this section is Ebix makes real cash flow. Since 2009 Ebix has:

Spent $786M on acquisitions

Returned $435M to shareholders

Increased its NWC (including cash balance) by $239M

Invested $150M in Capex

This has not been funded by accounting gimmicks but rather by:

Generating $805M of FCF

After paying $298M of interest

Ebix made $110M of UFCF last year)

Raising $539M of New Debt

Determining what segment that FCF came from is more difficult. The main way Ebix shifted profits between divisions was by overbilling internal software development contracts. Ebix’s US subsidiaries overbilled Ebix’s India subsidiaries (through Dubai based Ebix Asia Pacific FZ-LLC). The main thing to takeaway is that divisional accounting is a zero-sum game. Ebix took earnings from its right pocket and put them in its left pocket, but the company’s aggregate EBITDA is truthful. Matt Levine wrote an article on ADM a few weeks ago that mirrored this situation.

Without the internal overbilling, I estimate is that EbixCash’s true EBITDA was $47M in the twelve months preceding 3/31/2023. This compares to $136M of TTM EBITDA for the overall business as of 9/31/2023 adding back $6M of restructuring costs.

Taking out the $55M of EBITDA from the NA Life and Annuity Assets (Asset Purchase Agreement QoE) and the $47M of EBITDA from EbixCash leaves ~$34M for the remainder of Ebix’s businesses.

I expect a little more than half of the remaining $34M to come from international exchanges. The balance will come from the remaining US businesses, principally the certificate of insurance business.

The final thing to touch on is potential de-synergies. By directly hiring its own Indian software developers instead of contracting them through Infosys or Wipro (who have 20-30% gross margins) Ebix has vertically integrated its own business process outsourcing. EbixCash’s Financial Technology & IT Services segment spent $21M on labor. At the market rate, this service would be marked up to ~$30M (resulting in 30% gross margins), and there would be $9M of de-synergies.

I apologize if that was confusing, I tried to condense four months of research as tightly as possible. I am happy to go more into the weeds in the comments. I have tried to estimate divisional EBITDA from a few different angles and have gotten ballpark estimates close to the ones below every time. Most importantly, these estimates fall roughly in line with my margin expectations for each business segment.

To summarize EBITDA and Revenue Estimates by Division:

Path out of Bankruptcy

There is no equity committee because the judge ruled that although Ebix may be solvent, the interests of the equity holders were already adequately represented by the board, the Chief Restructuring Officer (CRO), and the Unsecured Creditors Committee. One good data point is that the CRO’s bonus is tied to an equity payout — a very unusual provision because equity payouts are rarely the expectation in bankruptcy. Another positive indication was that Director Geordie Hebard 5xed his stake. I have found no other cases of similar post-bankruptcy insider buying.

Nonetheless, being a passive investor in the junior class of a bankruptcy is dangerous. Here, however, the stakeholders are more aligned than in most bankruptcies. If all goes as it should, no one should be fighting over how the pie gets split up because the only two classes above the equity, the banks, and the unsecured trade claims, should be unimpaired. The banks, led by Regions, hold all the secured debt and are running the process here. Early in the process, they lent a small (but expensive) Debtor in Possession loan. This $23M DIP loan will be fully repaid along with $313M of the prepetition debt with the North American Life & Annuity proceeds. There remains $314M of debt, plus $15M of unsecured trade claims before the equity is in the money. Equity holders can gain further comfort from the fact that both classes want cash. There is no distressed debt fund trying to convert its debt to equity at a low valuation here. The equity should be the fulcrum security, to the extent there is one.

There are multiple avenues out of bankruptcy. Ebix will sell the remaining North American assets, but beyond, that Ebix could try to reorganize by refinancing its debt and potentially selling equity. However, the most effective solution to maximize the company’s value is to sell everything. The comps to the Indian business are shockingly high—Thomas Cook trades at 17x EV/EBITDA, EaseMyTrip at 37x, and MakeMyTrip at 90x. These multiples reflect optimism surrounding the secular tailwinds of Indian travel as well as an exuberant Indian market. An anecdote that illustrates this exuberance is that 84% of the options in the world were traded in India last year (up from 15% ten years ago). The number of retail investment accounts in India has tripled since 2019.

Selling the business is not only the only way for Ebix to monetize EbixCash at a high value, but whoever acquires EbixCash will probably get a good deal on a highly strategic asset. A former EaseMyTrip employee said,

"Ebix[Cash] would be a perfect fit for [a strategic acquirer] to dominate the entire travel market, online and off-line right? Now for me to tell you that MakeMyTrip would want to, it's not for me to say. That's their decision. But it will really, really give them a commanding position.”

Additionally, because Ebix’s cost basis is so high on the Indian assets selling them would create a loss that would offset the gain on sale from the North American Assets.

It’s also worth noting, the Restructuring Support Agreement has very unusual verbiage:

“the existing common interests of Ebix will be reinstated and will not otherwise be affected by the Restructuring Transactions, to the extent permitted by Law”.

This further reflects the expectation that there will be sufficient value to pay off all debt in full.

Finally, there are a lot of comps of businesses that retained equity value during bankruptcy and many of them were forced into bankruptcy for similar, liquidity driven reasons: Amerco (Uhaul), Alexander’s, Core Scientific, Hertz, and General Growth Properties. I would encourage anyone interested to Google Bill Ackman’s presentation on GGP—he also recently talked about it on a podcast.

Risks to the Ebix Investment Thesis

The $71M of remaining EBITDA is not all there.

The primary risk is the business may have deteriorated over the last six months since it filed financials. I am comforted by the periodic reports that have been filed that break down Ebix’s financials by LLC. Unfortunately, this is less useful than it sounds because it is clouded by intercompany transfers. Nonetheless, the topline results point to business stagnation but not deterioration. Additionally, Indian tourism and business travel have continued to rebound since the reporting date, so EbixCash would have to fall back against a strong tailwind.

Ebix has also underinvested in its non-Indian businesses and their earnings with a more normalized expense structure may be lower. This has been confirmed by former employees and customers. On Glassdoor, Ebix’s US offices have less than two stars, but its Indian offices have over four stars. It also can be seen in the US headcount numbers, which have decreased from 572 to 428 in the last five years, or the NA L&A segments 57% margin, which prioritized short-term profitability above long-term business sustainability. This may result in lower multiples than expected for the remaining non-Indian businesses.

I also could be underestimating the de-synergies.

I am misinterpreting the accounting.

The FCF gives me confidence. Additionally, in frauds that inflated profits, usually through hiding expenses via off-balance sheet entities a la Enron, the playbook has been to use the inflated earnings to issue stock or for insiders to sell stock. That has not happened at Ebix. Ebix has been a major repurchaser of stock and insiders have not been major sellers.

There is a contingent liability that has not been announced.

Most of Ebix’s acquisitions were structured with earnouts. EbixCash still must buy out 20% of ItzCash (one of its fintech acquisition) for $30M. Additionally, it has smaller earnouts it must pay, but they aggregate to less than $10M. Also, Ebix owes $33M to the Australian tax office payable between 2025 and 2028.

The final potential liability is gain on sale taxes from asset divestitures. There were $368M of assets in the US as of the 10k. Ebix’s tax basis is almost certainly less than that number, and Ebix will get more proceeds from the sale of its other US assets, which could leave a gain more than $200M and subsequently a $40M+ tax. I am hopeful this tax to be sidestepped by selling a high tax basis Indian asset (like Routier or ItzCash). If that does not happen, Ebix does have $35M of NOLs it can utilize to shield most of the tax leakage. However, the NOLs could be lost if there is a reorganization transaction that results in a change in control or if a new substantial shareholder emerges.

Shareholders lose out in the bankruptcy process.

To start bankruptcy is unpredictable, and I have tried to learn as much as possible about the process, but I don’t know what I don’t know. The basic idea here is equity holders are entitled to their pro rata share of the reorganized entity after all creditors have been paid. For example, if there is $50 still owed to creditors and an enterprise is worth $100 the creditors can either take 50% of the reorganized, unlevered entity, $50 in debt and $0 in equity, or sell off parts of the business until there is $50 in cash. I initially took comfort in the fact that Ebix’s creditors are traditional banks, not sharp elbowed distressed debt funds. However, the banks seem to be acting smart and somewhat aggressive here. There may need to be an equity rights offering, or a convertible preferred investment (like in Garrett Motion).

The management may not have Ebix’s best interest at heart, particularly in regard to selling assets. Richard Morgner, the Jeffries banker leading the reorganization mentioned the possibility of a management buyout by Robin Raina. Raina never sold a material amount of stock, so I don’t know where he would get the money from. Additionally, he owns a 14% stake in the company, which was pivotal in the Judge's decision to reject the motion for an equity committee, citing adequate representation.

Valuation

My valuation is as follows:

The two main assumptions here is that there is no dilution and that EbixCash is valued at 7.5x EBITDA. 7.5x EBITDA is a significant discount to Indian peers. For reference, EbixCash’s closest peer (and potential strategic acquirer) Thomas Cook India trades at 17x EBITDA. Thomas Cook has the second biggest airport forex exchange business in India and has various other travel related companies. Makemytrip is also a potential acquirer of EbixCash’s Travel business

A more optimistic pitch would point to Ebix’s median EBITDA multiple of 12x over the last ten years. This would result in a rebound to $19 a share.

Conclusion

Ebix is pretty clearly not a total fraud and its fundamental value also seems to be in excess of its debt. However, there is a lot of hair on this name, so to expect fundamental value to be reached is unrealistic. The bankruptcy process is rarely value maximizing and contains little regard for equity holders. The more I learn about this business the greater I appreciate the risk inherent in this situation. There are a lot of ways to lose here. There is a real possibility that the unaudited cross border nature of the business results in a broken process that fetches less than 4x EBITDA, which would result in Ebix’s equity is worth $0 in two months, so size it appropriately.

Disclaimer: This is not investment advice. Do your own due diligence. Bankrupt microcaps contain risk. At the time of publication, I hold an investment in Ebix that I may add to or close out of at anytime.

Well that didn't work. Good try though!

I'd meant to type up a long reply here, but didn't have the time. In short, I went through a lot of the Ebix travel websites, and looked at available pictures of their physical locations.

Per the Wayback Machine, the websites had barely been updated since their purchases. They still us the same version of various JavaScript libraries they did back when they were bought. The business storefronts are shall we say very unimpressive.

I think Raina's MO is buying companies, and not spending anything on upkeep. That generates strong cash flow, until it doesn't.

Doesn't seem like EbixCash had any value:

"With respect to EbixCash, Jefferies contacted over 70 parties with explicit interest in all or certain of the assets of EbixCash. 21 parties executed a non-disclosure agreement with the Debtors, and nine (9) parties interested in EbixCash executed a non-reliance letter with Deloitte for access of Deloitte’s draft vendor due diligence report.

Again, however, although the Debtors received interest in the EbixCash assets, the Debtors were not able to secure a transaction for these assets, including due to the EbixCash Liabilities, potential regulatory review and approvals for such a transaction, cash flow impacts from the sale of the North America assets, and significant working capital requirements for the EbxCash business."

Good well researched Article!

Your educated guess puts share price to fall upwards of $6 and, in best case lucky scenario, to reach $19.

Given a consortium, supposedly blessed by Raina et al, l stepped forward to buy EBIX outright without assuming liabilities, what are your thoughts on possible endgame, shareholders getting their money, etc.

Thanks!